If I Go - Bro

It is not easy for me to plan for the possibility of me not being in your life but it must be done. In this note I will work on what you should do if I am not able to help you with the money. I will try to update it as our life changes. The big picture is to simply keep things as simple as possible. Do your best to make no big changes until things have settled down and definitely do not make any changes you don’t fully understand.

1. The house:

It is up to you if you would like to keep our house. I know if you were not in the house it would be hard to call a home. You will need to pay HOA monthly, HOA twice a year (mailed to us twice a year), Taxes (once a year), and Insurance (xx insurance company, monthly automatic), gas (automatic), electricity(automatic), and water(automatic). The majority of these expenses are automatically deducted from our joint checking account or our shared credit card.

It is up to you if you would like to keep our house. I know if you were not in the house it would be hard to call a home. You will need to pay HOA monthly, HOA twice a year (mailed to us twice a year), Taxes (once a year), and Insurance (xx insurance company, monthly automatic), gas (automatic), electricity(automatic), and water(automatic). The majority of these expenses are automatically deducted from our joint checking account or our shared credit card.

2. The Car:

Both cars are paid for. Once a year you will need to pay taxes and once a year you will need to pay for insurance (xx insurance company, automatic). Do you best to do regular maintenance. If you need a new car just use the emergency fund to pay for it. Long term I would sell one of the cars in order to simplify your life.

Both cars are paid for. Once a year you will need to pay taxes and once a year you will need to pay for insurance (xx insurance company, automatic). Do you best to do regular maintenance. If you need a new car just use the emergency fund to pay for it. Long term I would sell one of the cars in order to simplify your life.

3. Credit Cards:

Cancel all but the xx bank Credit card. Pay the credit card off in full each month. I personally prefer to pay them off twice a month but once a month is fine.

4: Invest:

A large ($xx) life insurance policy should kick in if I pass away. Once things have settled down a bit I would invest the full amount into the stock market and live off the dividends as much as you can. The fund I would recommend is the Vanguard Total Market fund (VTSAX). If you are not comfortable with this you can take a year to learn more about investing and Vanguard. There is no rush.

5: Income:

My rule of thumb is you can use 3% of your investments as income each year and you should not run out of money. To be on the safe side I would do your best to live on only the dividends. Below is the order in which I would spend the money out of investments. If you do it right you should owe very low or no tax. As of now with life insurance invested you should have $xx a year in dividends that get deposited directly into your checking account every year. If you need more take only what you need. The dividends and social security should be enough to pay the bills but might not allow you to travel and go on adventures like we originally planned. The Social Security benefit should be $xx per child until they turn 18 and and $xx for you until the kids turn 16 but the total of those three payments cannot exceed $xx per month. In simple terms you should get $xx per month until youngest child turns 16, and then it will decrease to $2,140 per month until youngest child turns 18. Between these two sources of income you should have enough to live off of. If you find that you have a lot of extra money ($xx+) in your bank account for some reason just put it back into the stock market.

A) Deposit taxed dividends directly into your checking account. They should be about 2% of your investment value.

B) You might be eligible for some Social Security survivor benefit. Currently I estimate it to be up to xx per year.

C) Sell taxed stock in order to cover the rest of your expenses.

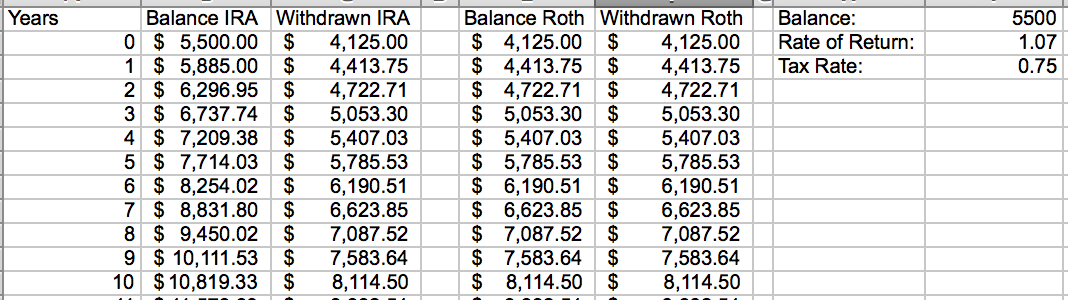

D) Use the hardship rule or the principal exemption of the Roth IRA to get access to this money.E) The 401K can be accessed after age 59.5. Our other investments should be enough to get you to this age.

6. Cabin:

I would do nothing with the cabin for one year. Use it as you would normally. Papa should be able to help if you have any maintenance issues or questions. After you have had a year to process the situation decide at that point if you want to keep the cabin. If you choose to not keep it sell the cabin and invest the money.

I hope my wife never has to use this letter but we both feel better knowing it exists. I update it as things change. Between this and Mint.com my wife should be able to continue without me. Please feel free to copy and modify for your own situation. The more prepared you are the better.

Comments

Post a Comment