IRA vs Roth IRA - Bro

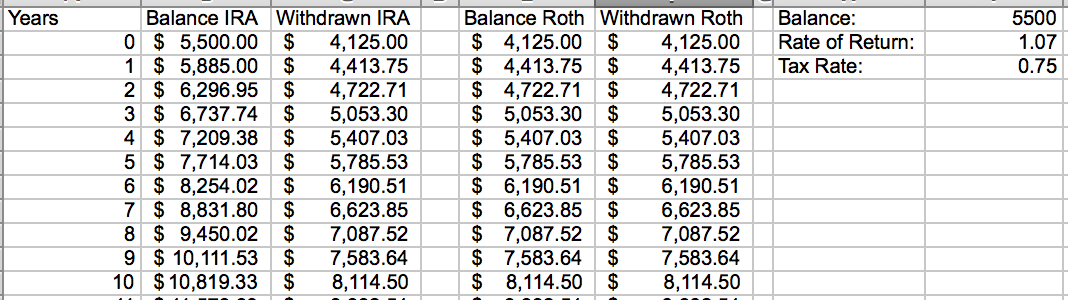

I recently had a reader question if a Roth IRA or a Traditional IRA is better. Of course the answer is (not) simple! All info contained in this blog post is to the best of my knowledge (and research). Please do your own homework before you make any money moves. Step 0 : What is a Roth or Traditional IRA ? Roth IRA: The money that you put in there is already taxed and is taken out without paying any more taxes*. EX: If you make 50,000 as a couple it would cost you $6,470 ($970 in taxes) to make the $5,500 contribution. When you get to retirement you will owe no taxes on what you take out. Traditional IRA: The money that you put in there is before taxes and when it is taken out it is taxed. EX: You make your $5,500 before you pay any tax on it. When you withdraw the money you pay taxes on it as if it were normal income. In this case if you were to withdraw $5,500 after the age of 60 and your income was 50,000 as a couple you would pay 15% tax or $825. There is...