Advanced E-Fund Ideas - Bro

In the first post I discussed how much money you need in your emergency fund. In the second post I discussed the standard places to put your emergency fund money. In this post I will discuss some alternatives to the traditional emergency fund.

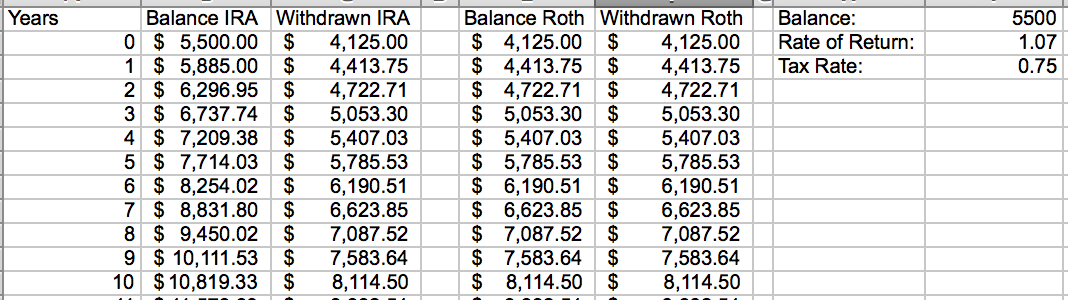

A Roth IRA is a type of account that allows you to invest after-tax dollars and not pay tax on your earnings. They can be a great deal if you are starting from a lower tax base (IE just starting your career) because it can save you lots of money in taxes. One of the things that makes Roth IRAs so powerful is you are allowed to withdraw the principal (the money you invested but not the earnings) at any time. This comes in handy for an emergency fund because you can fund a retirement account and have some money set aside in case of an emergency. It is the classic two birds with one stone. The money should be invested conservatively. This could be bonds or index funds. The best place to open an investing account is Vanguard. They have a great selection of mutual funds and lead the industry in being cost effective. The major downside to using this as an emergency account is if you withdraw your money from the account you can never put it back. This can damage your retirement plans for something that is a short term blip. In addition the account limits yearly contributions to $5,500 in 2017 and has income limits.

Another place emergency funds can be put is in taxed stocks (mutual fund). These are just your run of the mill offerings. Any principal that you remove is not taxed and gains are taxed at the more favorable capital gains tax rate if you let your money sit for long enough. Vanguard is also the best place to put your taxed account. If you are using the money for emergency savings the best place to put it would be in the total market index fund (VTSAX). The main consideration to a taxed account (in addition to a Roth account) is you can lose money. In the great recession stocks dropped by 50%. Due to this fact if you think you need 3 months of expenses as savings I would keep the equivalent of 6 months in the stock market so it could drop 50% and still leave you with enough money. One major downside to using stocks as your emergency fund is when the market goes down you are much more likely to need to use your savings. When the market crashes companies stop spending and lay people off. This can really be a double whammy. On the other side of the coin if you don't use your funds for a while they can have significant growth. Another factor is even if stock prices go down they still pay a dividend. If your savings are large enough the dividends could contribute a significant amount of money to your emergency money pool. An example of this is the mutual fund VTSAX pays about a 2% dividend. If you had $100,000 invested VTSAX would pay you $2,000 a year. $2,000 could be a month worth of living expenses if you are very careful.

The last type of emergency I consider very dangerous. This would be a line of credit. The most common version of this would be a line of credit on your home. This is basically a loan where you can borrow money at a certain agreed upon rate. If you run into a bit of trouble you can borrow the money and then pay it back like you would any other loan. The problem with this method is when you typically need the most money is when you can’t afford to make loan payments. You might find yourself in a position where you are borrowing money to pay back your loans. In the end the compounding interest will work against you and crush you. The benefit to using this method is you can payoff your home sooner if you can put your emergency fund towards paying off your loan instead of having your emergency fund in a low yield assets like a checking account.

These three alternative methods for emergency funds are some of the many options out there. I myself have used the Roth IRA in the past and still use the taxed stock accounts as a second line of defence. The best way to handle an emergency is to have a plan before it happens. These tools can help you prepare.

Comments

Post a Comment